Domain Asking Price vs Selling Price: Why the Listed Number Isn’t the Price | BuyerAxis

TL;DR

> A listed asking price on a premium domain is an anchor the seller has set — not what the domain will transact for.

> There is no fixed market price for premium names. They sell on what the name is worth to a specific buyer and how movable the seller is.

> Sellers of premium .coms have near-zero holding costs, so they can wait years. Time pressure sits with the buyer, not the seller.

> The number that closes a deal is discovered through the seller’s motivation — which can’t be read off a listing or a valuation tool.

> The fastest way to inflate the price is to reveal who’s buying. The gap between ask and close is largest when the buyer stays invisible.

Domain Asking Price vs Selling Price: Why the Listed Number Isn’t the Price

You found the domain. It’s listed at $250,000. Is that the price?

Almost never. An asking price on a premium domain is a positioning signal — a number the seller chose to shape how buyers think, not a figure anyone expects to be wired tomorrow. Understanding the gap between what a domain is listed at and what it actually transacts for is the single most useful thing a buyer can learn before entering a negotiation, because everything about how you approach the deal flows from it.

Table of Contents

Why is there no “market price” for a premium domain?

Commodities have market prices because units are interchangeable. Domains are the opposite — every name is unique, and its value is specific to whoever wants it. The same short, brandable .com can be worth four figures to one buyer and seven figures to another, depending on what they’re building, how central the name is to it, and what the alternative costs them.

This is why comparable sales, valuation tools, and “domains like this sell for X” logic all break down at the premium tier. Two names that look identical on paper — same length, same quality, same extension — have closed at wildly different numbers, because price isn’t a property of the domain. It’s a property of the negotiation: one specific buyer, one specific seller, on one specific day.

Anyone quoting a confident market price for a one-of-one asset is guessing. The honest answer to “what is this domain worth?” is always: worth to whom?

What is an asking price actually for?

An asking price does a job for the seller, and it isn’t “state the price.” It does three things.

It anchors. The first number in any negotiation pulls every later number toward it. A $250K ask makes $120K feel like a discount, even if the seller would have taken $80K from the right anonymous buyer.

It filters. A high ask screens out casual inquiries and signals the seller isn’t desperate. Sellers of genuinely premium names would rather field three serious conversations a year than three hundred lowballs.

It signals patience. A premium .com renews for the cost of a lunch. The seller’s carrying cost is effectively zero, which means the ask can sit unchanged for years without pressure. Buyers routinely assume a listed domain that hasn’t sold must eventually come down. It doesn’t have to — and with strong names, it usually doesn’t.

None of those three jobs requires the ask to be realistic. That’s why it so often isn’t.

So what actually determines the selling price?

The number a deal closes at is set by variables that never appear on the listing.

The seller’s motivation is the biggest one. A seller who just renewed a 500-name portfolio and needs liquidity behaves completely differently from one holding a single trophy name as a retirement asset. Same ask, entirely different floor. Motivation shifts with time, circumstances, and how the approach is handled — which is why it has to be read directly, not inferred from the listing.

What the name is worth to you is the second. Not what a tool says, not what a comparable sold for — what having this name versus settling for an alternative is worth to your business. That number is your ceiling, and it’s the one piece of information a buyer should establish privately before any contact and never reveal.

Who the seller thinks is buying is the third, and it’s the one that moves price the most violently. The moment a seller senses a funded company behind an inquiry — or worse, a company whose brand matches the name — the price detaches from market logic entirely and starts tracking the buyer’s perceived wallet. A name that would have closed in five figures from an anonymous individual can become a six-figure ask overnight once the seller knows who wants it. That repricing is permanent. You cannot un-ring the bell.

Why does the buyer usually lose the waiting game?

Buyers often decide to wait the seller out: the ask is absurd, nobody will pay it, the seller will soften. Sometimes true. Usually not, and for a structural reason — the holding economics run one way.

The seller pays a few dollars a year to hold the asset indefinitely. The buyer, meanwhile, is usually building something: a launch approaching, a brand compounding on the wrong extension, marketing spend accumulating on a name they intend to leave. Every month of waiting costs the buyer real money and costs the seller nothing. Time is on the seller’s side, and experienced sellers know it.

This doesn’t mean overpaying now beats waiting. It means “wait for the price to drop” is a strategy that needs an actual mechanism behind it — a motivated seller, a portfolio liquidation, a failed alternative buyer — not just hope. Absent a mechanism, waiting is a plan to pay more later.

How do buyers close below the ask?

The gap between asking price and selling price is where a disciplined acquisition operates. The levers are consistent.

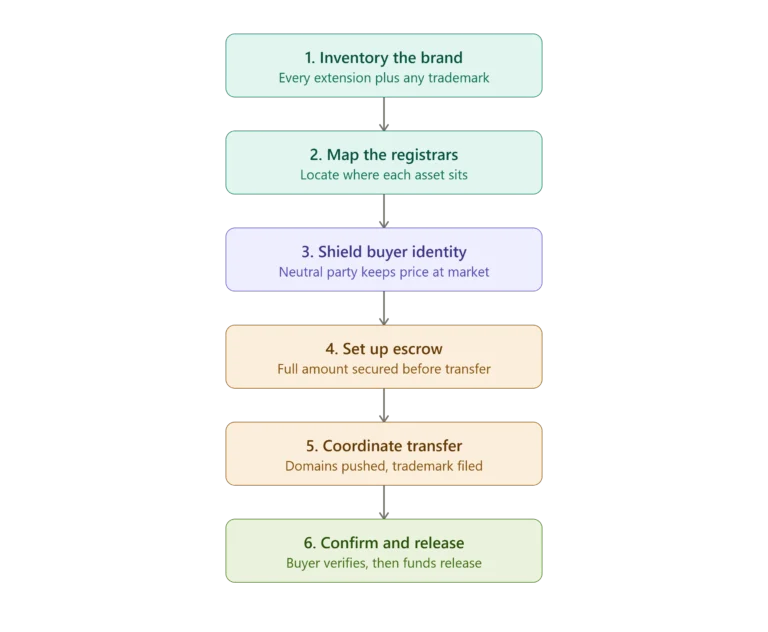

Anonymity first. Every point above compounds into this one: the ask-to-close gap is largest when the seller cannot price against the buyer. A neutral approach, with no trace back to the real buyer, keeps the negotiation anchored to the asset instead of to a budget. This is the entire reason buyerside acquisition exists as a discipline.

Reading motivation before talking numbers. The first conversations with a seller aren’t about price — they’re about establishing why this seller holds this name and what would move them. The opening number should be set after that read, not before it.

Structure when the gap won’t close on price alone. Lease-to-own, installments, and deferred structures can bridge a real gap between a seller’s floor and a buyer’s ceiling — a deal that won’t close at $60K cash can sometimes close at $75K over eighteen months, and both sides come out ahead of no deal. Structure widens the solution space, but it bridges gaps of degree, not gaps of kind: terms won’t turn a $250K seller into a $50K seller.

Willingness to walk. The buyer who must have the name has already lost the negotiation. A genuine alternative — a different name, a modified brand — is the quietest leverage in the room, and sellers can tell when it exists.

Do domains ever sell at the asking price?

Sometimes — usually when the ask was set realistically low to move the name fast, or when a strategic buyer decides the name is worth it and speed matters more than savings. On premium names with aspirational asks, transaction prices routinely land meaningfully below the listed figure. The ask is where negotiation starts, not where it ends.

Why do sellers list unrealistic prices?

Because the ask costs nothing and does useful work: it anchors negotiations high, filters out non-serious buyers, and loses the seller nothing while they wait. With renewal costs of a few dollars a year, there’s no pressure forcing the number toward realism.

Should I just offer half the asking price?

Formulas like “offer 50% of ask” assume the ask carries information about the seller’s floor. It usually doesn’t. The right opening depends on the seller’s motivation and the name’s realistic range — an offer that’s insultingly low can end the conversation or, worse, signal desperation when you return higher. The opening number is a strategic decision, not a percentage.

How do I find out what a domain will really sell for?

You can’t read it from the outside — not from the listing, not from valuation tools, not from comparables. The real number emerges from contact with the seller: their responsiveness, their flexibility, what moves them. That’s why the approach matters more than the analysis, and why it should be made by someone who doesn’t reveal who’s actually buying.

Does the seller knowing my identity really change the price?

It’s frequently the single largest price factor in the whole transaction. Sellers price against the buyer they can see. An anonymous inquiry gets a market conversation; a funded company with a matching brand gets a strategic-value conversation. The difference is routinely multiples, not percentages.

Wondering what a specific domain would actually take?

The ask is public. The real number isn’t. We assess targets confidentially — who holds the name, whether they’ll genuinely sell, and what it would realistically take to close — with your identity protected from first contact onward. We represent buyers only.